Ember’s data

The data for this report is based on Ember’s yearly and monthly electricity dataset.

You can find the full methodology for underlying emissions, generation and capacity data here. Yearly and monthly electricity data is available for download in Ember’s data catalogue.

Fuel saving esstimate

The formula to estimate the amount of fossil fuel saved by solar energy under various scenarios can be downloaded here.

The avoided costs are estimated based on each country’s actual power generation data for January to June 2022 from Ember’s Data Explorer. The potential avoided costs in 2030 uses the target solar generation of each country in 2030, as presented in their National Energy Plans.

The thermal efficiency of power plants is extracted from IEA World Energy Balances, and detailed in the table below:

| Country |

Coal |

Gas |

Oil |

| China |

38.0% |

56.6% |

35.0% |

| India |

36.8% |

40.6% |

16.8% |

| Malaysia |

34.0% |

43.1% |

14.3% |

| The Philippines |

31.9% |

54.1% |

41.9% |

| South Korea |

38.3% |

55.1% |

39.3% |

| Thailand |

36.9% |

46.0% |

32.9% |

| Viet Nam |

30.9% |

50.7% |

49.6% |

Thermal efficiencies in Japan were not available in the original dataset; the thermal efficiency of plants in South Korea was used.

Net calorific value (NCV) of imported fuels is also considered, as the volume of imports would have likely had to increase if additional solar was unavailable. These NCVs are obtained from IEA World Energy Statistics, and detailed below.

|

Coal

Bituminous coal |

Natural Gas

|

Oil

Diesel oil |

| China |

20.9 |

46.9 |

44.6 |

| India |

23.6 |

49.9 |

44.6 |

| Japan |

23.8 |

47.6 |

44.6 |

| Malaysia |

26.4 |

47.3 |

44.6 |

| The Philippines |

22.1 |

46.5 |

44.6 |

| South Korea |

23.7 |

50.3 |

44.6 |

| Thailand |

26.4 |

43.9 |

44.6 |

| Viet Nam |

23.4 |

46.6 |

44.6 |

Assumed Net Calorific Value of fossil fuels in MJ/kg.

According to the UN Comtrade Database, most of the steam coal (i.e. excluding coking coal) imported in these countries is bituminous coal. We therefore used the NCV of bituminous coal. We also assume that oil power generation is using diesel oil, with a NCV of 44.6 MJ/kg.

Solar/fossil fuel substitution

To estimate the amount of fuel saved by solar electricity generation, one needs to build a counterfactual scenario where the solar electricity generation is generated by other fuels instead. Here we assume that solar has replaced incumbent fossil fuel based electricity generation. For our estimation to be conservative, we assume solar has replaced the cheapest form of fossil-fuel based generation during that period (i.e. either coal, gas or oil) and for each country independently.

However, we use different assumptions for Indonesia. We assume solar has replaced oil first, then the cheapest form of fossil-fuel based generation during that period, as stated by the Ministry of Energy and Mineral Resources and PLN (state-owned utility company).

Fossil fuel prices

Fossil fuels are sold on a variety of contracts including fixed-price, indexed to average oil prices and indexed to other spot prices. This means that the price of fossil fuel is not directly proportional to the current spot price, and it may vary from one country to another.

UN Comtrade database provides trade data in both physical and monetary terms, allowing us to derive a monthly commodity price for each country separately. Commodities considered for t.

However, at the time of writing, 2022-H1 trade data is not available for every country (see table below).

|

Coal |

Gas |

Oil |

| China |

March 2022 |

March 2022 |

March 2022 |

| India |

July 2022 |

July 2022 |

July 2022 |

| Indonesia |

March 2022 |

March 2022 |

March 2022 |

| Japan |

August 2022 |

August 2022 |

August 2022 |

| Malaysia |

December 2021 |

December 2021 |

December 2021 |

| The Philippines |

June 2022 |

June 2022 |

June 2022 |

| South Korea |

December 2019 |

December 2019 |

December 2019 |

| Thailand |

December 2020 |

December 2020 |

December 2020 |

| Viet Nam |

December 2020 |

December 2020 |

December 2020 |

Latest available dates in UN Comtrade Database at the time of writing.

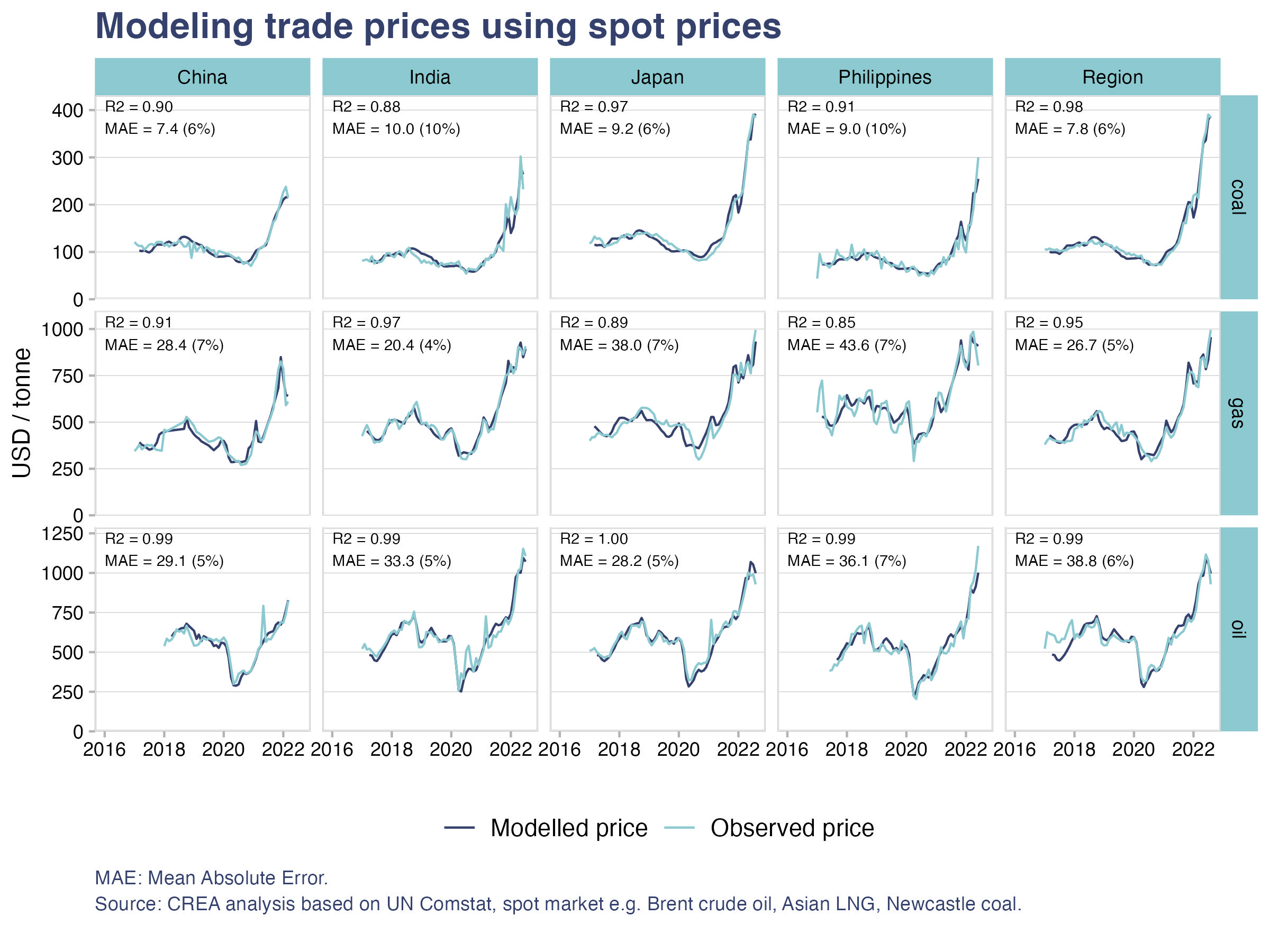

To estimate prices of displaced fossil fuel trades in 2022, we build linear regression models between historical prices and average monthly spot prices for the current month and with lags (Brent crude oil, TTF gas, Asian LNG, Newcastle coal futures). Models are built for countries individually (see Figure 2).

Commodities considered and their corresponding HS code are listed in the table below:

|

HS code |

HS description |

| Coal |

270112 |

Coal, bituminous. |

| Gas |

2711 |

Petroleum gases and other gaseous hydrocarbons. |

| Oil |

2710 |

Petroleum oils and oils from bituminous minerals, not crude. |

Malaysia, South Korea, Thailand and Viet Nam have not yet reported 2022 data. Therefore, the models for these countries did not capture the unusually high prices in 2022-H1. To prevent this from affecting results, the average fuel prices for the region was assumed for these countries. To further prevent model drift (i.e. model prediction beyond the domain it was trained on), we cap commodity pricing using the highest observed prices in the region.

The quality of model fitting is relatively good, with typical R squared greater than 0.9 and median absolute error within 10% of average price. Modelled trade prices chart can be downloaded here.

Prices in 2030

Avoided fuel cost estimates in 2030 use 2019 (low) and 2022 (high) commodity pricing as a reference for 2030 prices.

Bloomberg New Energy Finance

BNEF datasets were used in the financial and investment section of this report, which are available on this link. This is a paid service and will need a subscription to access. To subscribe, please contact BNEF on https://about.bnef.com/.

{kind=link}

{kind=link}