Summary for Policymakers

Emergent Themes

Main conclusions drawn from the modelled pathways

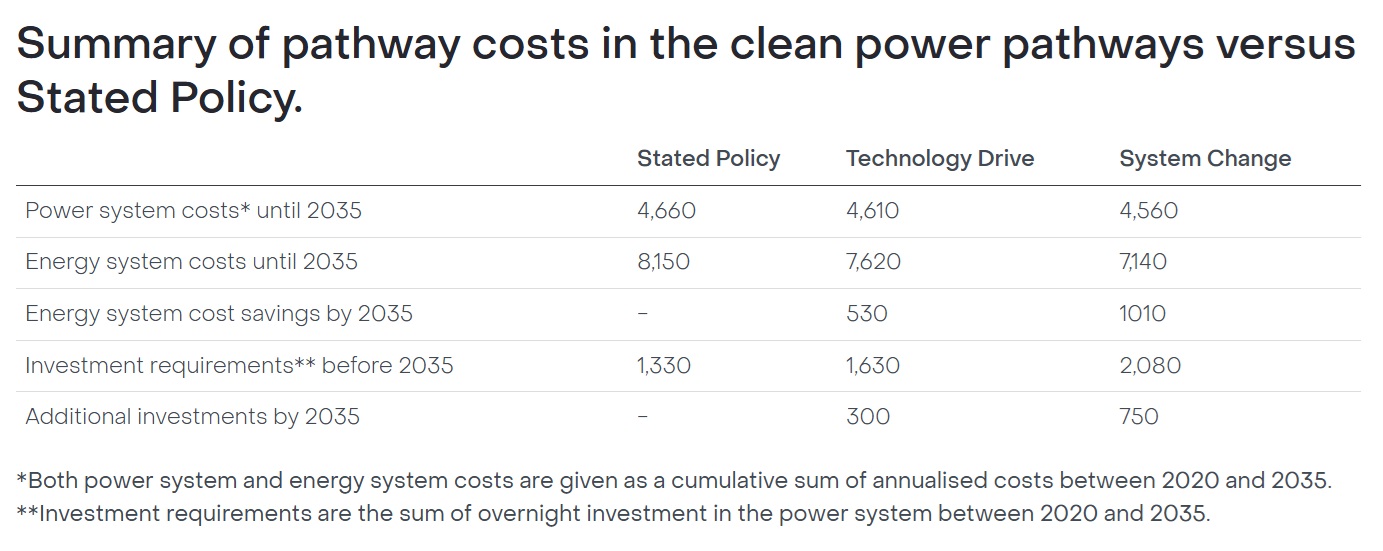

Clean power is cheaper than stated policies

An expanded and (~95%) clean power system in Europe can be achieved by 2035 at no extra cost above stated plans.

Larger upfront capital costs for wind and solar in the power system are offset by avoided carbon costs and avoided costs associated with new nuclear and fossil capacities.

The additional electricity (and green hydrogen) supply unlocks further electrification in the economy, leading to substantial cost savings of €530-1010 billion in total by 2035 as a result of avoided fossil fuel consumption. This is likely an underestimate as the unprecedented increase in fossil fuel prices in 2021-2022 are not taken into account. The expanded power supply in clean power pathways allows direct electrification to reach 40-47% by 2035, compared to 30% under Stated Policy.

As a result of expanded supply and lower costs, the price of electricity in clean power pathways is lower than in Stated Policy. By 2035 the average cost of electricity in clean power pathways is 23-30% lower than under stated policy.

Building a clean, wind and solar dominated power system by 2035 will require an additional upfront investment of between €300-750bn above existing plans. While larger upfront investment is needed, mostly in wind and solar, these are strongly justified by the cost savings which are rapidly realised (as stated above), as well as benefits to climate, health, and energy security.

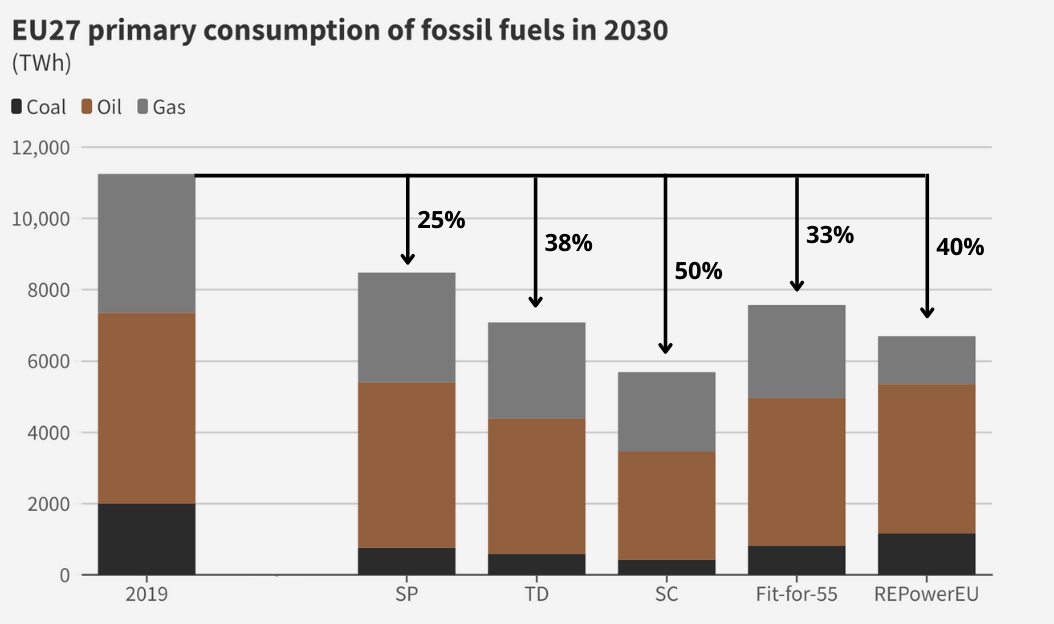

Fossil fuel consumption halves this decade

The EU27 is highly dependent on imports of all major fossil fuel types. This state of high exposure to price-volatile energy sources poses a clear risk to the EU27’s energy sovereignty and economic stability. Pursuing an energy system based on domestic renewables presents a safer path with better outcomes for European consumers.

A combination of clean electrification and energy savings can reduce Europe’s (and EU27) fossil fuel consumption by up to 50% by 2030, improving energy sovereignty.

The modelled clean power pathways would reduce total fossil fuel consumption in Europe (and the EU27) by an estimated 38-50%. This is compared to an estimated 25% reduction under stated policies. The Fit-for-55 plan, if implemented, would reduce EU27 consumption by 33%. The REPowerEU plan, which represents increased ambition above Fit-for-55, reduces consumption by 40%. REPowerEU is particularly focused on gas consumption which in 2030 is halved compared to the Fit-for-55 plan. However, this is at the expense of additional coal consumption in 2030, and little extra progress on oil reduction.

Electrification contributes to approximately 70% of fossil fuel reductions.

Electrification of end uses often delivers major efficiency improvements compared to conventional use of fossil fuels. This is most obvious in the case of space heating (heat pumps) and light-duty transport (electric vehicles), which represent the low-hanging fruit for decarbonisation through electrification. Direct and indirect electrification, combined with the efficiency savings from these technology switches, deliver approximately 70% of estimated fossil fuel reductions by 2030. The remainder are delivered through energy savings, primarily from building renovation and modal shift in transport, showing that societal change also has a role to play.

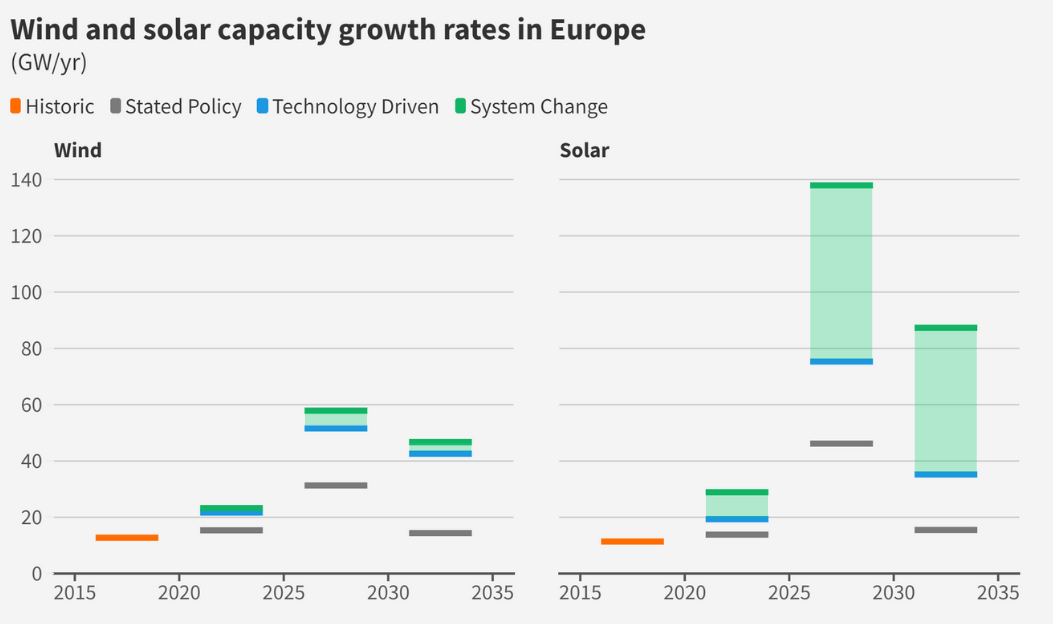

Wind and solar deployment quadruples

Annual growth in wind and solar capacity must quadruple by 2025 compared to the last decade; this is the central challenge to deliver a clean power sector by 2035.

Over the period 2025-2035 the combined deployment rate should reach 100-165 GW per year, compared to an annual growth of 24 GW per year between 2010-2020. There are signs of acceleration, with additions hitting a record 36 GW in 2021, but a big deployment challenge lies ahead. Meeting the challenge requires permitting times to be slashed, and supply chains and manufacturing capacity to be secured. In least-cost pathways Europe’s wind fleet quadruples to 800 GW by 2035, and solar expands 5-9 fold reaching 800-1400 GW.

Required solar deployment aligns with ambitious industry estimates, but wind deployment would need to exceed industry’s best expectations.

The required growth rates in solar (55-115 GW per year), coincide with ambitious industry estimates that EU27 expansion can reach 53-90GW/yr by 2025. In contrast, the required wind growth (47-52 GW per year) is significantly higher than best case industry estimates, which forecast just 18GW per year (EU27) by 2025.

Stated policies would deliver just 45-65% of the wind and solar capacity required by 2035. Ambitions for 2030 set out previously by the European Commission as part of the Fit-for-55 package would also fall short. However, the recently announced REpowerEU plan goes a long way to closing the gap between stated ambition and the modelled pathways to 2035 clean power. While this is encouraging, major challenges remain in translating this higher ambition into European and national policy, and deploying the infrastructure on the ground.

Wind and solar become the backbone

In the least-cost pathways, wind and solar provide 70-80% of the electricity supply by 2035.

Such high shares of wind and solar are robust to sensitivity analysis, demonstrating a clear cost benefit to maximising the contribution of wind and solar. Stated Policy puts these technologies on track for a 52% share by 2035. While the increased penetration of wind and solar does present challenges to system operation, there are some important (and sometimes overlooked) complementarities that benefit system operation.

Wind and solar outputs are complementary over a range of timescales.

Studies have shown that a degree of complementarity exists between wind and solar outputs over timescales of hours to months for many regions in Europe. Key to exploiting these natural patterns is the development of flexibility solutions, and notably interconnection, to create a more dynamic system capable of balancing temporal and geographic imbalances.

Wind and solar deliver across a large fraction of the year.

While there are some periods in the year where wind and solar output are anomalously low (see main finding 6 for analysis of a dunkelflaute period), there are many hours of the year where wind and solar provide or exceed total demand at the system level. At such times, excess generation can be shared between regions, or converted into hydrogen through electrolysis, or stored for later use. Enabling these routes with the right infrastructure is vital to maximising the value of renewables output.

System operators must start planning and adapting now for very high instantaneous shares of wind and solar. There are lessons to be learned from countries that already regularly manage this.

A paradigm shift in power system operation is needed, as an increasing share of weather-dependent sources means the system must become more responsive to available supply rather than demand. Maintaining system stability will require new approaches, as unlike conventional generation, wind and solar are variable on short timescales and have a non-synchronous interface with the grid. Technical studies and real world experiences are accumulating, and evidence suggests that engineering and technical challenges can be overcome. Some parts of the European grid already regularly operate with close to 100% renewables – Portugal and Denmark have experienced periods of instantaneous wind and solar exceeding 100% of demand.

Increasing flexibility is crucial

Enabling demand flexibility and deploying key power technologies facilitates the cost-efficient integration of wind and solar, while avoiding unnecessary gas investments.

As the power supply transforms into one dominated by wind and solar, a parallel system transformation is required to provide for their distinct flexibility needs, and to efficiently integrate new types of power demand. Maximising system flexibility reduces dependence on thermal (gas) capacities for balancing.

Electrification provides challenges but also opportunities if demand-side flexibility (such as smart charging EVs and flexible heat pumps) and battery storage, including that carried by electric vehicles, can be activated. This is particularly important for the integration of solar power, as shifting demand by a few hours can boost alignment with daylight hours.

Three key technologies emerge as the cornerstones of flexibility in a clean power system, maintaining system balance over a range of temporal scales: electrolysers, interconnections, and clean dispatchable generation.

The electrolyser fleet grows to 200-400 GW by 2035 and supplies 14-27Mt of green hydrogen, enough to cover the majority of estimated European domestic demand while maximising the value of renewables output. The REPowerEU plan broadly puts the EU27 on track for this by 2030, aiming for more than 65 GW of electrolyser capacity and 10Mt of hydrogen production.

Total interconnections at least doubles by 2035 compared to 2020, enabling the cost-efficient expansion of wind and solar capacities by allowing their deployment in countries with the most favourable conditions.

New clean dispatchable power sources enter the system by 2035, but the complete replacement of declining fossil and nuclear capacities is not required. As such, the general trend is towards a smaller and cleaner fleet of dispatchable sources by 2035, despite increases in electricity demand (and peak demand).

A clean system is reliable and resilient

A highly renewable power system is reliable and resilient even to extreme weather events.

Granular modelling reveals that Europe can operate a 95% clean power system by 2035 without compromising reliability and that the weather-dependent, variable nature of wind and solar does not pose a threat to the resilience of the grid. This remains the case with unfavourable climatic conditions – the 2035 clean power system is stress-tested using a year notable for both record low temperatures and severe heat waves (2010).

Resilient to a simultaneous cold spell and dunkelflaute.

The modelled ~95% clean power system delivers through a harsh cold spell – which drives up power demand – and a simultaneous prolonged reduction in wind and solar (dunkelflaute). Even during this period, there remains a sizeable contribution of wind and solar (~30%) at the system level, because it is exceedingly rare for meteorological events to affect the entirety of the European power system simultaneously. The successional impact of unfavourable weather conditions moving over Europe highlights the importance of interconnections in alleviating regional or national supply tightness.

Resilient to the hottest summer days.

Large solar capacities on the system lead to extreme daily supply variations, and increased cooling demand is expected in a warming climate, meaning summer months can also present challenging conditions. This modelling shows that a greater alignment of hourly supply and demand can be created through a combination of demand shifting (especially electric vehicle charging), storage, and electrolysis, successfully managing solar output that would otherwise far exceed demand.

Limited room for new fossil fuel capacity

Coal must be phased out by 2030 and unabated gas reduced to <5% of generation by 2035 to make Europe’s power system fit for the Paris Agreement.

This study agrees with multiple previous analyses that coal must be phased out by 2030. Any use beyond this – with the possible exception of a small reserve fleet – is neither cost-competitive nor compatible with climate goals. For similar reasons, unabated gas contributes only 4-6% of Europe’s power supply by 2035. The outlook could be worse if gas supply pressures and price volatility persist.

No new baseload (unabated) gas plants need to be commissioned beyond those expected by 2025.

Planned investments in baseload (unabated) gas power stations are currently higher than what is needed for clean power by 2035. While the conventional gas fleet maintains a role in balancing until 2035, stated plans deliver an estimated 60 GW of excess baseload gas assets. Instead, least-cost pathways see no expansion beyond what is expected by 2025. After this, investment quickly pivots away from baseload to peaking capacities, at least until low or zero-carbon gas capacities become available in the 2030s.

Bringing forward investment in clean dispatchable technologies can remove the need for any new unabated gas investments after 2025, with minimal impact on costs. If all deployment of unabated gas (peaking and baseload) stopped after 2025, the resulting shortfall in dispatchable capacity could be compensated by earlier investment in hydrogen turbines, gas with CCS and utility-scale batteries, at minimal extra cost.

A smaller and cleaner dispatchable fleet

Reductions in fossil capacity do not need to be fully compensated by growth in clean dispatchable capacities.

As a result, the total dispatchable fleet declines over time, which is perhaps unexpected given that electricity demand (and peak demand) increases over time. New clean dispatchable technologies – gas CCS and hydrogen turbines – enter the system by 2035 in sufficient quantities to compensate for the decline in nuclear, resulting in a similar sized but more flexible clean fleet.

The composition of the dispatchable fleet may take a variety of forms and still achieve clean power by 2035. The technology choices present different risk profiles, but estimated cost differences are minimal.

New nuclear is found not to be a cost-competitive option in clean power pathways. However, sensitivity analysis reveals that economic cost does not significantly distinguish between pathways using (or not) different clean dispatchable technology options. This includes a scenario in which new nuclear is developed in line with national plans, and a scenario in which CCS technology is not available. Instead of cost, decisions require balancing different risk profiles.

The wind and solar deployment challenge is largely unaffected by choices between dispatchable capacity options, which have greater implications for Europe’s dependency on fossil gas.

None of the alternative pathways explored – from additional nuclear to an absence of CCS technology – significantly change the wind and solar deployment requirements by 2035. This confirms that deploying wind and solar, plus supporting power system infrastructure, is the central challenge for power sector decarbonisation. The composition of the dispatchable fleet has a more notable impact on the consumption of natural gas in the power sector. In 2035, alternative clean power pathways with i) no gas CCS or ii) new nuclear (in line with current plans) see reductions of 13% and 15% in gas consumption respectively.

Related Content