3 The lasting consequences

Beyond the immediate shock, this crisis will reshape energy markets in three ways.

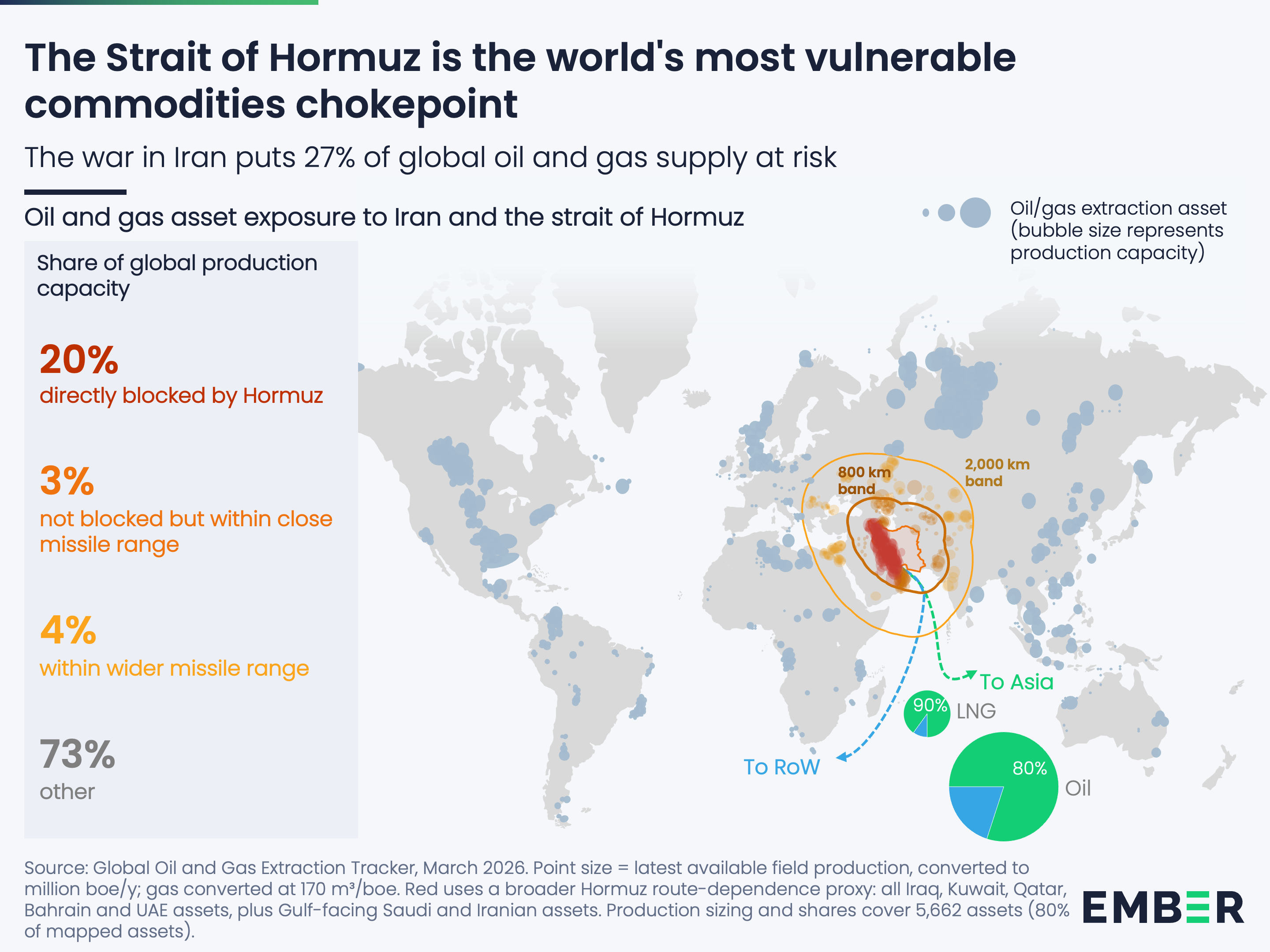

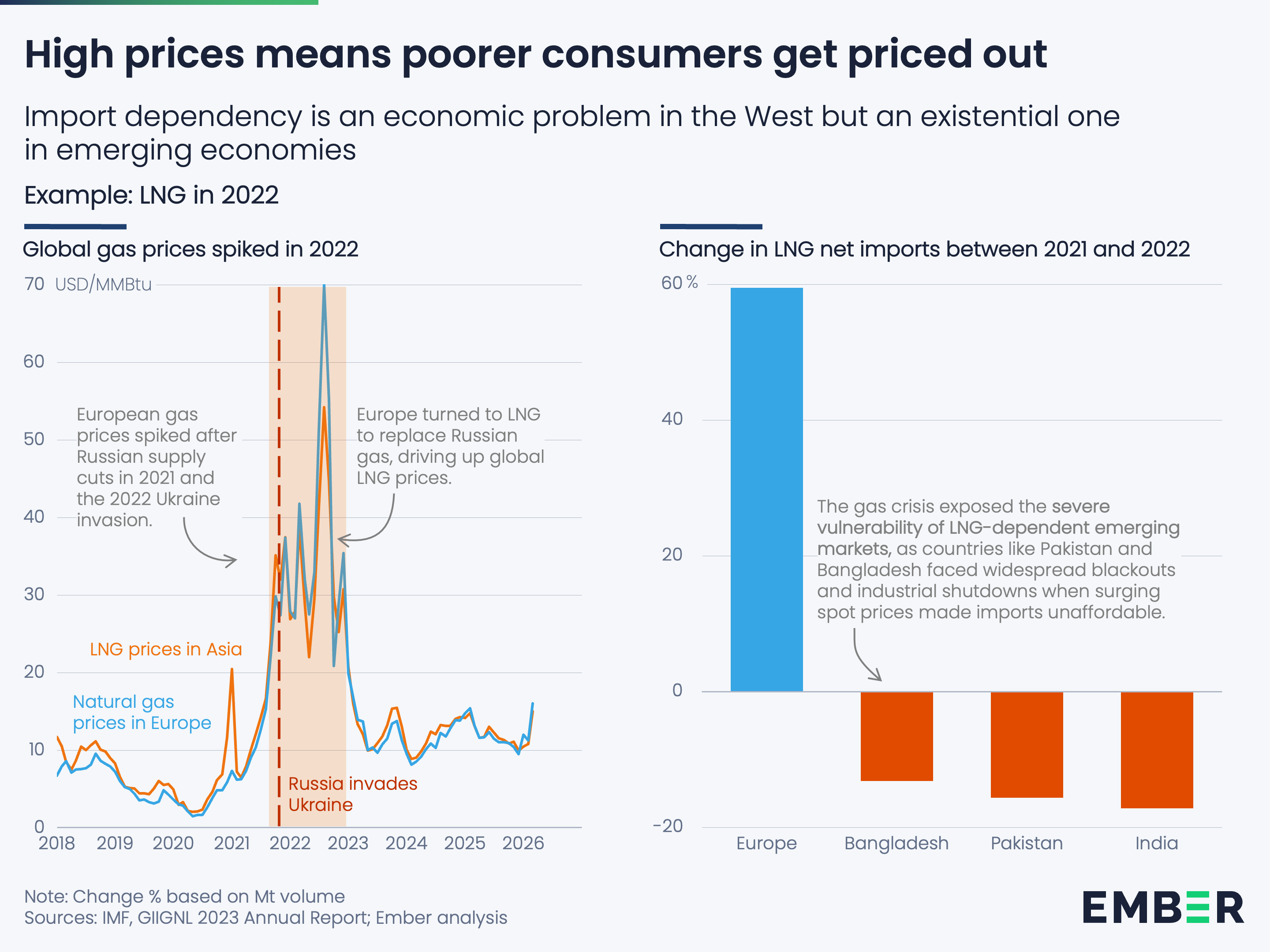

This is Asia’s Ukraine moment

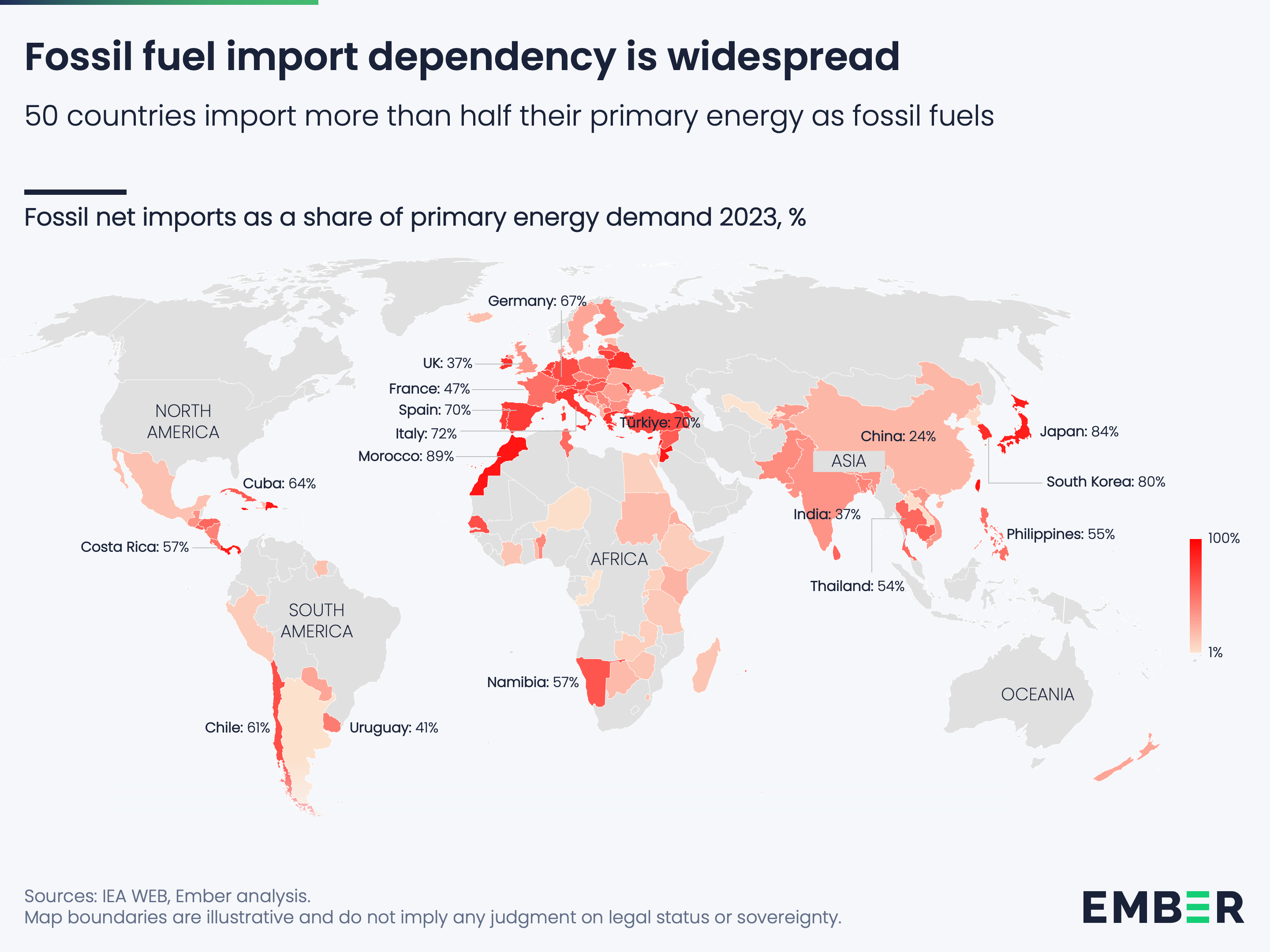

Russia’s invasion of Ukraine that began in 2022 galvanised Europe into action to reduce its dependency on Russian fossil fuels. Four years later, the US-Israel war with Iran will inspire Asia to reduce its dependency on imported oil and gas. The numbers are similar: in 2021 Europe imported around a third of its gas demand from Russia; in 2025 Asia imported 40% of its oil demand through the Strait of Hormuz.

But Asia enters this moment with an advantage that Europe did not have. Solar, wind, batteries and EVs are much cheaper and more readily available than they were in 2022, making the switch far more affordable. And where fossil fuel imports leak money out of the economy indefinitely, building up domestic electrotech manufacturing keeps that spending at home. Countries like India and Viet Nam are already showing the way. For Asia, this is not just a crisis to weather but an opportunity to convert fossil dependency into economic strength.

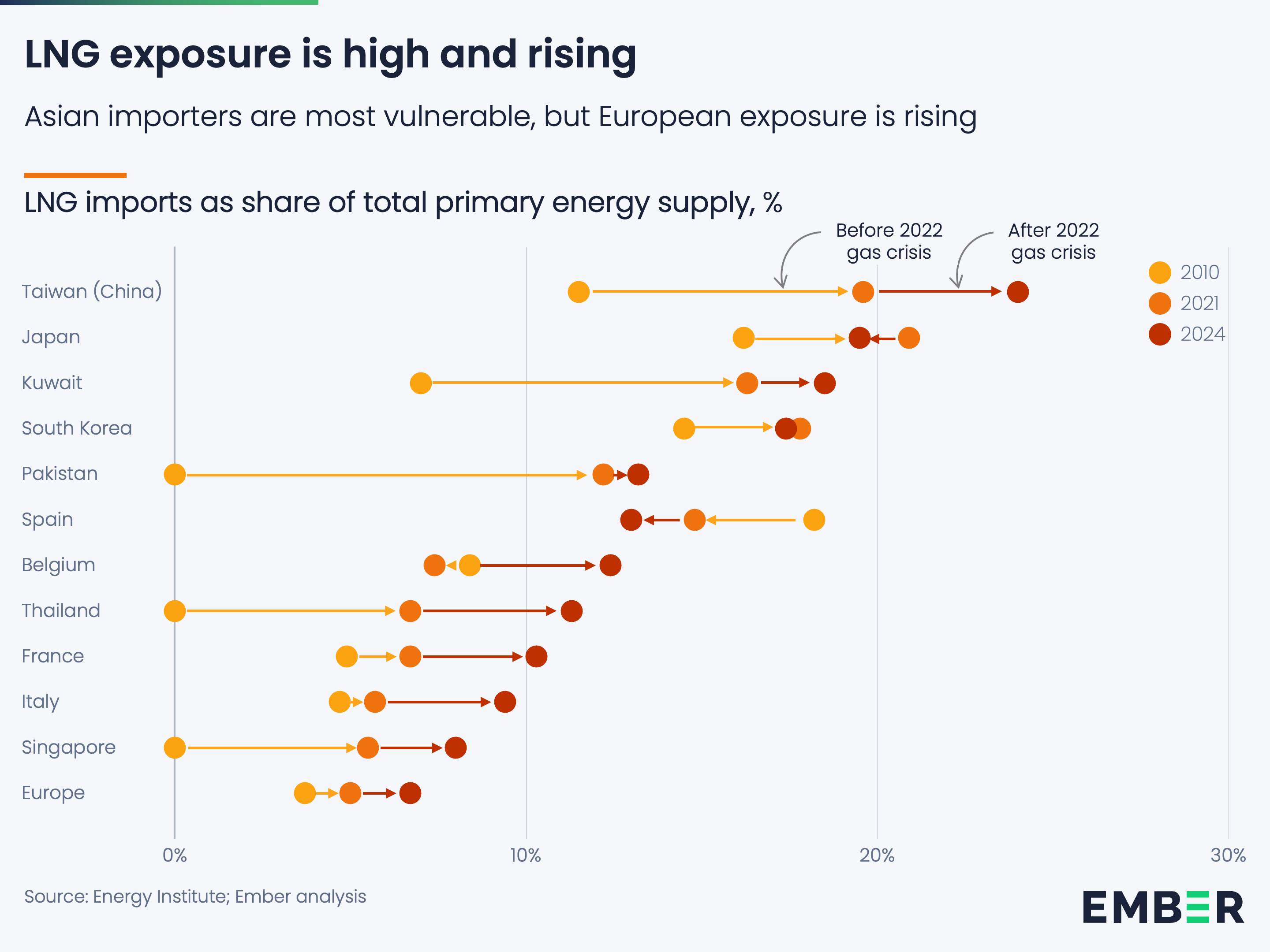

The prospects for LNG demand growth in Asia are over

As we noted last year in our Electrotech Revolution report, there is a battle between gas and solar for the future of electricity generation in Asia. At a stroke, this war has dramatically weakened the case for LNG.

The bull case for LNG was that it would be Asia’s transition fuel: cleaner than coal, available at scale, and secure. That thesis is now much weaker. Countries will be carefully considering the security of building long-term import infrastructure around a commodity that can see dramatic price spikes and supply risks.

Meanwhile, the alternative is already cheaper. Thanks to the collapse in solar and battery prices, Asia can now buy dispatchable solar at less than $80/MWh, with no fuel cost and no price risk, versus LNG at prices set by the next geopolitical crisis. Existing long-term LNG contracts become a liability, not an asset.

Peak oil demand is coming forward

For years, the International Energy Agency has been bringing forward its view of when oil demand will peak. A decade ago, it saw no peak before 2050 at all. Then it forecasted the late 2030s, and then 2030. Its latest forecast put it at 2029, at around 106 million barrels per day (mbpd), not much above 2025 levels of 104 mbpd. Even China, the largest growth market for oil over the past decade, saw demand fall in 2025 as electric vehicles displaced consumption.

This crisis is accelerating that trajectory. It is both curbing oil demand directly and sharpening the incentive to move away from oil altogether. The IEA has already cut its 2026 oil demand growth forecast to just 0.6 mbpd, and that is unlikely to be the last revision. As so often, a crisis can bring a peak sharply forward. We may well be at that peak now, in 2026. For a while, demand may simply bounce along that level. But if the closure of the Strait of Hormuz is prolonged, the plateau may turn quickly into structural decline.

Conclusion

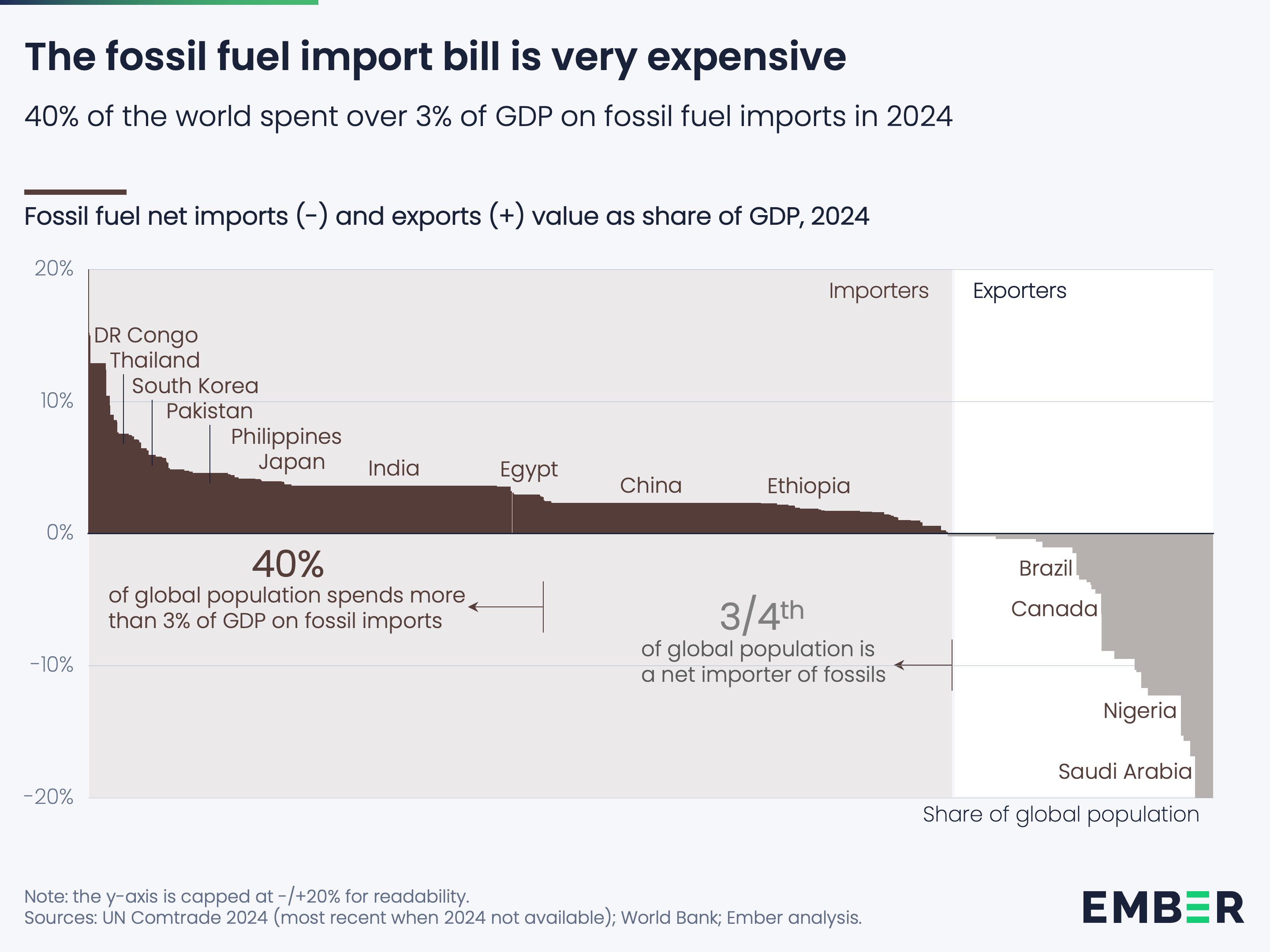

At some point the Strait of Hormuz will reopen. Prices will ease. The crisis will fade from the headlines. But the structural logic will not change, and the next disruption will not be long in coming. Every year of continued fossil fuel import dependency is another year of exposure to a system that has shown, repeatedly, that it cannot be relied upon. The technology to end that dependency exists. The only question is how many more crises it takes. The countries with the foresight to invest in electrotech now will be better able to weather the next storm.