If the defining economic story of the century is the rise of Asia, the defining energy story is the rise of electricity. The two are usually told apart. This report argues they are one: Asia’s rise is electric, and the electric age hastens Asia’s rise.

Electricity has been the century’s fastest-growing energy carrier, overtaking oil in 2007 as the leading supplier of useful energy worldwide. Over the same years, Asia has been the fastest-growing region. In 2016, China passed the United States in purchasing-power terms, and South and Southeast Asia together passed the European Union in 2021. Two features bind these stories together.

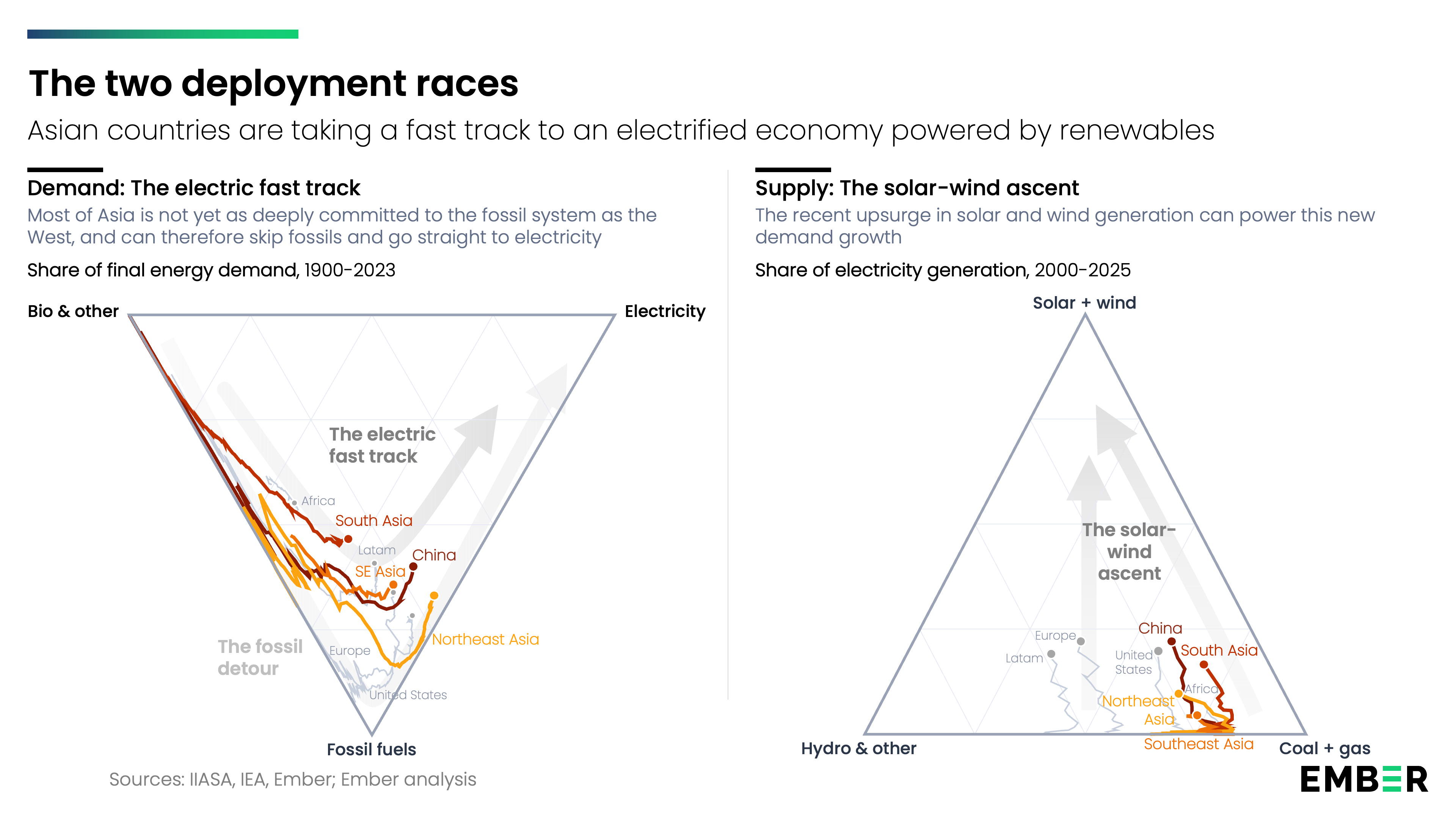

The first is that Asia is taking an electric path. Since the turn of the century, Asia has driven three quarters of the growth in global electricity. In the West, GDP and electricity demand decoupled long ago; in Asia, they rise in lock-step. Asia has achieved greater electrification at lower incomes per capita. No growth in history has been this electric.

The second runs deeper. It is a change in what energy is. Coal, oil and gas are commodities, dug from the ground. Solar panels, batteries and wind turbines are technologies, built on a production line. The energy revolution is the shift from extraction to manufacturing.

Enter Asia – the world’s factory. Asia builds most of the world’s solar panels, batteries, power electronics, electric motors and cars. Its strengths fit the new energy system.

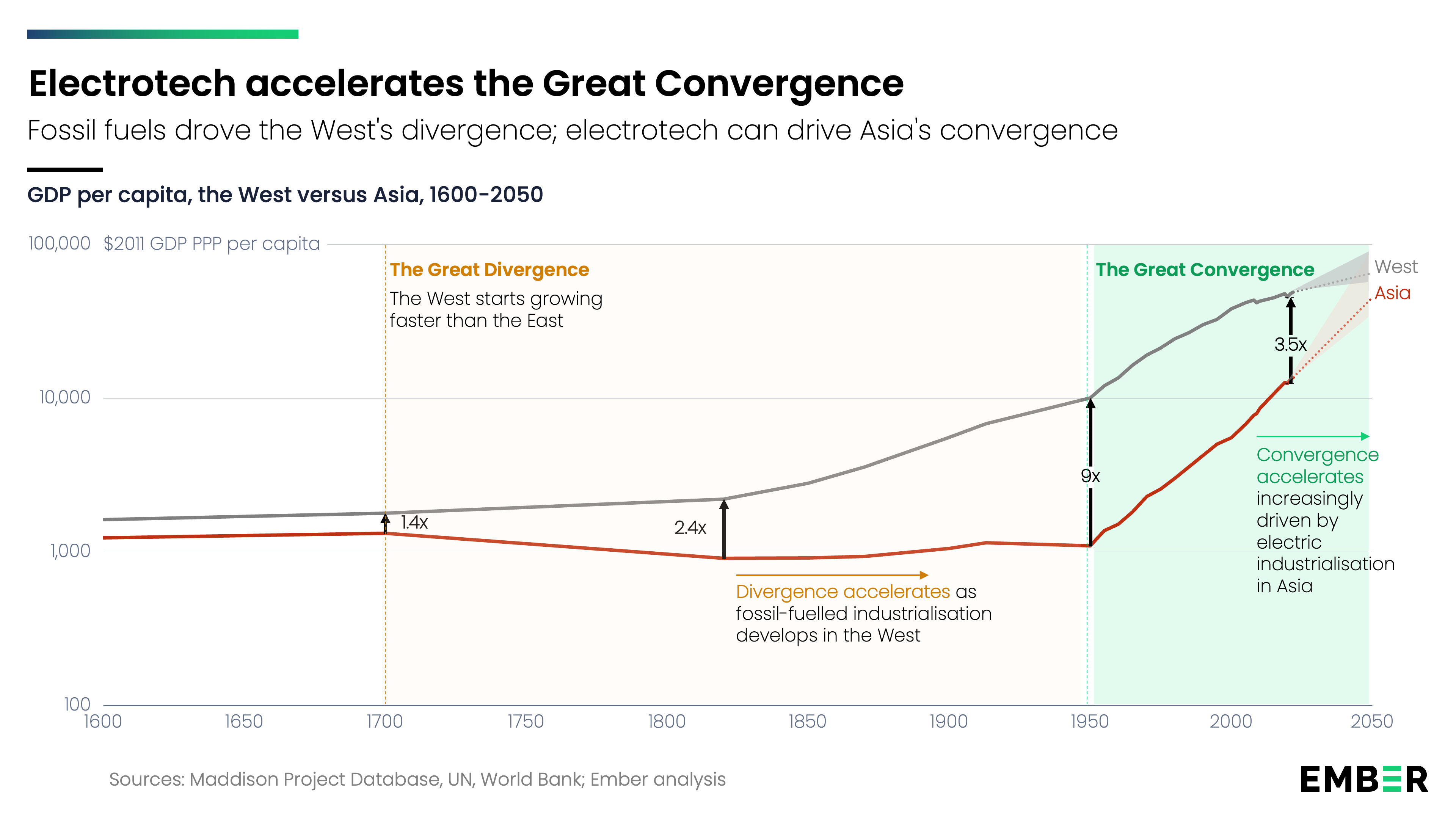

Such a shift carries historical weight. After 1800 the West pulled ahead of Asia, a parting of fortunes known as the Great Divergence. Energy sat at the core of this divergence: first coal, then oil, and the engines built to burn them. These innovations favoured Western strengths and underwrote two centuries of wealth and power.

The Great Convergence – the East closing in on the West – also has an energy story, and it runs the other way. The new vector is electricity, and the electro-technologies that run on it. The new centre is Asia. Its lack of oil and gas was a weakness in a fossil world. It is a blessing in an electric one.

China is, of course, the giant. But change is radiating outwards. From Vietnam to Bangladesh, electrification rates are higher than in Europe or the United States. From Pakistan to Japan, solar’s share of power beats the US. From Thailand to Nepal and Indonesia to Singapore, EV uptake is ahead. Strip China out, and the rest of Asia still outbuilds the world in solar modules and battery components.

For years the economics of electrotech have been improving rapidly. A decade ago, solar began to beat coal, and electric cars beat petrol over their lifetimes, once fuel was counted. Today solar and EVs are cheaper to buy outright, even before the fuel savings. For economies short of capital, the door is now open to rapid change.

Then came Hormuz: the closure of Asia’s petrol station. The region buys nearly half of its oil from the Gulf, a deeper reliance than Europe had on Russia. It is the second blow in four years. The first came in 2022, when Russia cut off Europe, and Europe outbid Asia for gas, pricing out poorer countries. If electrotech is the pull of opportunity, the twin fossil shock is the push of necessity.

Economics, security and industrial opportunity now all point in the same direction. Asia holds half the world’s people and 4% of its oil and gas, but three quarters of the electrotech factories that can replace the fuel it lacks. The Great Divergence was powered by the energy the West mastered. The Great Convergence runs on the energy that Asia manufactures. If this is to be the Asian century, its path will be electric.